Starting a business in Ireland offers key advantages, including a strategic location, favorable tax policies, and a pro-business environment. Both EU and non-EU residents can easily form companies through services like House of Companies' Entity Management, which ensures compliance with legal and administrative requirements. Ireland also provides tailored support for non-residents, ensuring a smooth setup process.

Choosing the right business structure is crucial for success in Ireland. Popular options include Sole Proprietorship, Partnership, Limited Liability Company (LLC), and Public Limited Company (PLC). An LLC offers limited liability and flexibility, while a PLC suits larger businesses aiming to raise capital. Understanding these options helps you choose the best structure for your business goals.

Company Registration Process in Ireland

The Process to Register a Company in Ireland

Registering a company in Ireland involves several key steps and interactions with various government agencies. The Companies Registration Office (CRO) is the primary body responsible for company registration. One of the first tasks is choosing a suitable company name and verifying its availability through the CRO’s website.

Next, you will need to prepare the necessary documentation, including the company constitution (formerly known as the memorandum and articles of association). Once your documents are ready, you’ll submit the required forms and supporting documents to the CRO, along with the registration fee.

After successful processing, you will receive your certificate of incorporation. This process is fully online via the CRO’s CORE (Companies Online Registration Environment) system, making it easy and efficient for both residents and non-residents. House of Companies offers entity management services to guide you through this process, ensuring a smooth registration experience. For detailed information and to start your registration, visit the official CRO website.

How Fast Can I Set Up My Company in Ireland?

The timeline for setting up a company in Ireland can vary depending on the complexity of your business and the completeness of your application. However, Ireland is renowned for its streamlined company registration process, making it an attractive destination for entrepreneurs looking to establish a business swiftly. For a standard company registration, the process typically takes between 5 to 10 working days.

If you need to expedite the process, Ireland offers a fast-track registration service, which allows you to complete the setup in just 5 working days, subject to an additional fee. It’s essential to ensure that all documentation is correct and complete, as any errors or omissions could delay the process.

To ensure a seamless and fast registration, it’s advisable to review all forms and documents carefully before submission. The House of Companies provides expert entity management services to help streamline the registration process, ensuring your company is set up quickly and efficiently in Ireland.

Selecting the Right Legal Structure for Your Business in Ireland

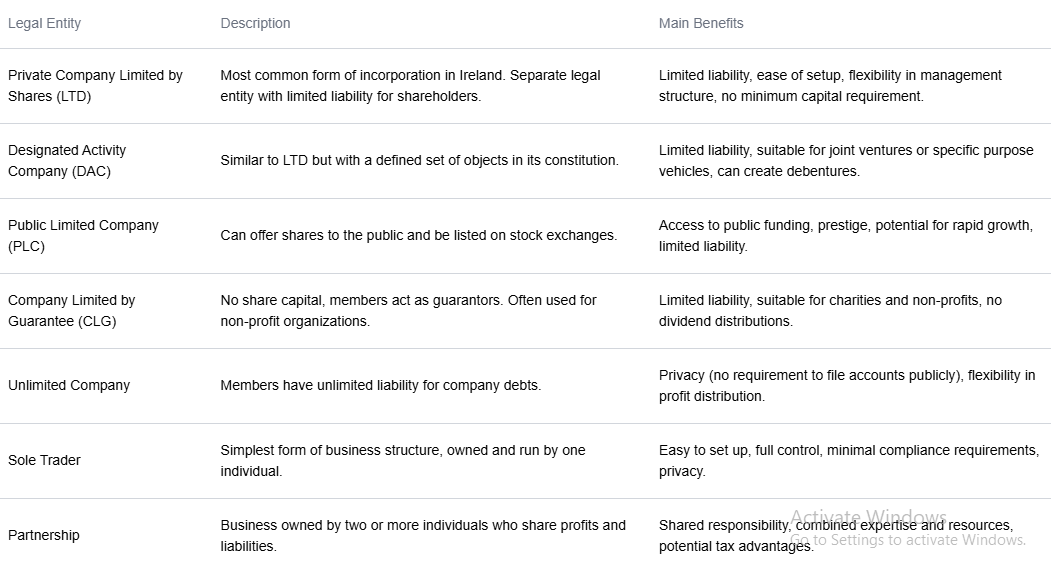

When setting up a business in Ireland, one of the first decisions you’ll face is selecting the right legal structure. The choice of business entity depends on factors such as the scale of your operation, tax implications, and regulatory requirements. Common structures include the Private Limited Company (LTD), Designated Activity Company (DAC), Public Limited Company (PLC), Unlimited Company, and the Branch of a Foreign Company.

A Private Limited Company (LTD) is the most common choice due to its limited liability protection, making it suitable for most businesses. On the other hand, establishing a Branch of a Foreign Company allows foreign entities to have a presence in Ireland without the need to set up a separate legal entity. It’s crucial to understand the advantages and challenges of each structure to ensure it aligns with your business goals.

The House of Companies provides comprehensive entity management services to assist you in selecting the optimal legal structure for your business. Their expert team can guide you through the nuances of each structure, ensuring you make an informed decision that supports your long-term business objectives.

Considerations for Non-Residents Establishing a Company

Non-residents looking to establish a company in Ireland should be aware of several key considerations. Firstly, at least one director of the company must be a resident of the European Economic Area (EEA). If this requirement can’t be met, you’ll need to secure a non-EEA resident director bond, which typically costs between €2,000 and €3,000.

Secondly, regardless of where the directors or shareholders are based, the company must have a registered office address in Ireland. This address will be used for official communications and must be a physical location in Ireland, not just a P.O. box.

Thirdly, compliance with Irish tax laws and regulations is essential. This includes registering for taxes, filing annual returns, and maintaining proper financial records. Lastly, while it’s possible to manage much of the company remotely, having a local presence or representative can be beneficial for day-to-day operations and ensuring ongoing compliance with local laws and regulations.

What Legal Entities Can You Form in Ireland? Let’s Find Out the Best for Non-Residents!

For non-residents, the most common and suitable legal entities in Ireland are the Private Limited Company (LTD) and the Branch of a Foreign Company. A Private Limited Company offers limited liability, which means the personal assets of shareholders are protected from the company’s debts. This structure is suitable for most businesses and is relatively straightforward to set up and maintain.

It also provides a strong foundation for growth and can easily accommodate additional shareholders or investors in the future. On the other hand, a Branch of a Foreign Company allows foreign companies to establish a presence in Ireland without creating a separate legal entity. This can be advantageous if you want to maintain closer control from the parent company or if you’re testing the Irish market before fully committing to a separate entity.

The choice between these depends on your business goals, tax considerations, and operational needs. It’s worth noting that while these are the most common choices, other structures like the Designated Activity Company (DAC) might be more suitable in specific scenarios, particularly if your business has a specific purpose or requires certain restrictions on its activities.

How to Open a Business in Ireland as a Branch Registration

Registering a branch of a foreign company in Ireland involves a specific process designed to establish your presence while maintaining the link to the parent company. The first step is to submit Form F12 to the Companies Registration Office (CRO) within 30 days of establishing the branch. This form requires detailed information about both the parent company and the Irish branch.

Along with Form F12, you’ll need to provide certified copies of the parent company’s constitution and certificate of incorporation. These documents should be in English or accompanied by a certified translation. You’ll also need to submit details of the branch’s directors and secretary.

Once you’ve gathered all the necessary documents, you’ll need to pay the required registration fee. After successful registration, your branch will be issued a unique registration number, separate from the parent company’s number. It’s important to note that while a branch is not a separate legal entity, it must comply with Irish reporting and tax requirements. For more detailed information on branch registration and ongoing compliance requirements, you can visit the CRO’s foreign company page on their official website.

Branching Out. Simplified.

Company Formation Details

Drafting the Articles of Association

The Articles of Association is a crucial document that outlines the company’s internal rules and procedures. This document serves as a constitution for your company, defining how it will be run and governed. When drafting the Articles of Association, there are several key points that need to be included. First, you’ll need to specify the company name and registered office address.

Next, you should detail the share capital structure and shareholders’ rights, including voting rights and procedures for transferring shares. The document should also outline the powers and responsibilities of the directors, including how they are appointed and removed. Decision-making processes for both the board of directors and shareholders should be clearly defined.

Additionally, it’s important to include procedures for conflict resolution and any specific rules unique to your company’s operations. Given the legal importance of this document, it’s highly advisable to seek legal assistance when drafting the Articles of Association. A legal professional can ensure that the document complies with Irish company law and adequately protects the interests of all parties involved.

Appointing Directors and Shareholders

When appointing directors and shareholders for your Irish company, there are several important factors to consider. First and foremost, ensure that at least one director is a resident of the European Economic Area (EEA). If this isn’t possible, you’ll need to secure a non-EEA resident director bond. In addition to directors, you’ll need to appoint a company secretary. This role can be filled by one of the directors if there’s more than one, or it can be a separate individual or corporate entity.

Next, you’ll need to determine the number and type of shares to be issued. This decision will impact the company’s capital structure and the rights of different shareholders. You’ll also need to identify the initial shareholders and their shareholdings.

It’s crucial to remember that directors have legal responsibilities and must comply with Irish company law. This includes duties such as acting in the best interests of the company, exercising independent judgment, and avoiding conflicts of interest. When appointing directors, consider their skills, experience, and ability to fulfill these legal obligations. It’s also worth noting that while there’s no legal maximum number of directors, the Articles of Association may specify a limit.

Registering with the Ireland Business Register

Registration with the Ireland Business Register occurs automatically upon incorporation with the Companies Registration Office (CRO). Once your company is successfully registered, it is assigned a unique Company Registration Number (CRN). This number is essential for all official communications and filings and is required when interacting with other government agencies, such as the Revenue Commissioners for tax purposes.

Responsibility for Accurate Information While registration with the Business Register is automatic, it is your responsibility to ensure that the information provided during the registration process is accurate and up to date. If there are any changes to your company's details, such as a change in directors or the registered address, these must be promptly reported to the CRO to maintain compliance.

Public Accessibility of Company Information The Ireland Business Register is a public record, meaning that basic information about your company, including its name, registration number, and registered address, will be accessible to the public. This transparency is designed to facilitate business transactions and instill confidence in potential partners or customers.

Register for Tax Purposes

Register for Corporation Tax After incorporation, one of the first crucial steps is to register your company for tax purposes with the Revenue Commissioners. The first tax registration you'll need to complete is for Corporation Tax. This is mandatory for all companies incorporated in Ireland, regardless of whether they are actively trading. It's important to ensure that this registration is done promptly, as it establishes your company's tax obligations in Ireland.

Register for VAT If your business turnover is expected to exceed the VAT threshold—currently €75,000 for goods or €37,500 for services in any 12-month period—you must also register for Value Added Tax (VAT). Even if you don't anticipate reaching this threshold immediately, you can choose to register voluntarily if it would benefit your business. VAT registration is an important step in ensuring compliance with Ireland's tax laws and can help streamline the way you manage your business’s finances.

Register as an Employer If you plan to hire staff, you'll need to register as an employer with the Revenue Commissioners. This registration is required even if you are the sole employee of your company. The good news is that all these tax registrations can be completed online via the Revenue Online Service (ROS). ROS provides a convenient platform for managing your tax affairs, including filing returns and making payments. It's advisable to complete these registrations as soon as possible after incorporation to ensure your company is fully compliant with Irish tax laws from the outset.

Register for PAYE (if employing staff)

If you’re planning to employ staff in your Irish company, you must register as an employer and operate the Pay As You Earn (PAYE) system. This process involves several steps and ongoing responsibilities.

First, you need to register as an employer with Revenue. This can be done through the Revenue Online Service (ROS) and should be completed before you start paying wages to any employees. Once registered, you’ll need to set up a payroll system. This system should be capable of calculating the correct deductions for each employee, including PAYE (income tax), PRSI (social insurance), and USC (universal social charge).

These calculations can be complex, so many employers choose to use payroll software or outsource this function to a payroll service provider. As an employer, you’re required to calculate and deduct these amounts from your employees’ wages and remit them to Revenue. You must also submit payroll information to Revenue on or before each payday. This is done through the PAYE Modernised system, which requires real-time reporting of payroll data.

It’s crucial to ensure that all payroll submissions are accurate and timely to avoid penalties. For detailed guidance on employer obligations and how to comply with the PAYE system, you can visit the Revenue’s Employer’s Guide to PAYE on their official website.

Choose Your Business Structure (e.g., Sole Trader, LTD, Partnership)

Choosing the right business structure is a crucial decision that will have long-term implications for your business. In Ireland, the main options are Sole Trader, Limited Company (LTD), and Partnership, each with its own advantages and considerations.

A Sole Trader structure is suitable for individuals operating alone. It’s the simplest to set up and manage, with minimal paperwork and regulatory requirements. However, it doesn’t provide limited liability, meaning your personal assets could be at risk if the business incurs debts.

A Limited Company (LTD) offers limited liability, protecting your personal assets from business debts. It’s suitable for most businesses and can enhance your professional image. However, it involves more complex setup and ongoing compliance requirements, including annual financial statements and returns.

A Partnership is appropriate for two or more individuals or companies sharing ownership. It allows for shared management and pooled resources but, like a sole tradership, doesn’t offer limited liability unless it’s a Limited Liability Partnership.

Each structure has different legal and tax implications. For instance, a sole trader pays income tax on profits, while a limited company pays corporation tax. The choice of structure should be based on factors such as the nature of your business, your growth plans, the level of personal liability you’re comfortable with, and your tax situation. Given the significance of this decision, it’s advisable to consult with a legal or financial professional to choose the structure that best suits your business needs and future plans.

Request the Guide

Sign up by completing the form below.

Thank You, we'll be in touch soon.

Financial and Tax Considerations

Company registration costs in Ireland

The costs associated with company registration in Ireland are relatively straightforward, but it’s important to budget for both direct and indirect expenses. The primary cost is the CRO registration fee, which is €100 for standard registration.

However, if you choose to register online, the fee is reduced to €50, providing a cost-effective option for many new businesses. If you want to reserve a company name before full registration, there’s an optional name reservation fee of €25. While these are the basic costs, it’s crucial to factor in additional expenses that may arise during the registration process.

Many businesses choose to engage professional services for legal and accounting advice during setup. These fees can vary widely depending on the complexity of your business structure and the level of assistance required. If your company doesn’t have an EEA-resident director, you’ll need to secure a non-resident director bond, which typically costs between €2,000 and €3,000.

Lastly, if you plan to operate under a business name different from your company name, you’ll need to register this separately. The fee for business name registration is €20 for online filing or €40 for paper filing. While these costs may seem significant, they’re a one-time investment in establishing your business on a solid legal footing in Ireland.

Benefits of the Ireland Tax System

Ireland’s tax system offers several significant benefits that make it an attractive location for businesses, particularly for international companies and startups. One of the most notable advantages is the low corporate tax rate of 12.5% on trading income.

This rate is one of the lowest in the European Union and has been a key factor in attracting foreign direct investment to Ireland. For income from non-trading activities, such as passive income from investments, a higher rate of 25% applies. Ireland also boasts an extensive network of double taxation agreements with over 70 countries.

These agreements help prevent the same income from being taxed twice in different jurisdictions, which is particularly beneficial for companies operating internationally. For businesses engaged in research and development, Ireland offers a generous R&D tax credit. This credit provides a 25% tax credit on qualifying R&D expenditure, which can be offset against corporate tax liability.

Another attractive feature is the Knowledge Development Box regime, which offers a reduced tax rate of 6.25% on profits derived from certain types of intellectual property. Lastly, Ireland’s treatment of foreign dividend income is favorable, with many foreign dividends taxed at the 12.5% rate. These tax incentives, combined with Ireland’s skilled workforce and access to the EU market, make it an attractive location for a wide range of businesses.

Tax Benefits For Entrepreneurs Starting A Business In Ireland

Entrepreneurs starting a business in Ireland can take advantage of several tax benefits designed to support new ventures. One significant incentive is the Start-up Relief for Entrepreneurs (SURE). This scheme provides a refund of income tax paid in previous years to individuals who leave employment to start their own business.

The relief is available for up to €100,000 of previous income tax paid. Another valuable incentive is the Employment and Investment Incentive (EII). This scheme offers tax relief for investors who purchase new shares in certain corporate trades. It can be an excellent way for startups to attract investment, as it allows investors to claim relief of up to 40% of their investment.

For entrepreneurs looking to sell their business in the future, the Capital Gains Tax Entrepreneur Relief offers a reduced CGT rate of 10% on qualifying business disposals, up to a lifetime limit of €1 million in chargeable gains. This can significantly reduce the tax burden when exiting a successful business. The Research and Development Tax Credit is another valuable benefit, offering a 25% tax credit on qualifying R&D expenditure.

This can be particularly beneficial for tech startups or any business investing in innovation. These tax benefits, combined with Ireland’s supportive ecosystem for startups, make it an attractive location for entrepreneurs to launch and grow their businesses. For more detailed information on these benefits and how to qualify, entrepreneurs can visit the Revenue’s Tax and Duty Reliefs page on their official website.

Financial Reporting and Audit Requirements in Ireland

Irish companies must comply with financial reporting and audit requirements to ensure transparency and accountability. These requirements vary based on the company’s size and type, but all must maintain accurate books of account to record transactions and determine the financial position.

Companies are required to prepare annual financial statements in accordance with either IFRS (International Financial Reporting Standards) or FRS (Financial Reporting Standards). Small companies may be eligible to prepare abridged financial statements under the small companies regime.

In addition to the financial statements, companies must file annual returns with the Companies Registration Office (CRO), including basic company information and financial statements. These must be filed within 28 days of the company’s annual return date.

Audit requirements depend on the company’s size. Small companies may qualify for audit exemption if they meet two of the following thresholds: annual turnover of €12 million, balance sheet total of €6 million, and 50 employees. However, even exempt companies may choose to audit their financial stateme

Operational Aspects

Opening a Business Bank Account

Opening a business bank account is a crucial step in establishing your company’s financial operations in Ireland. It’s not only a legal requirement for most business structures but also essential for maintaining clear financial records and separating personal and business finances. The process of opening a business bank account in Ireland is governed by the Criminal Justice (Money Laundering and Terrorist Financing) Act 2010, as amended, which requires banks to conduct thorough due diligence on new customers.

To open a business bank account, you’ll typically need to provide:

Certificate of Incorporation (for limited companies) or business registration documents (for sole traders or partnerships)

Company’s Constitution (formerly Memorandum and Articles of Association)

Proof of identity and address for all directors, significant shareholders, and beneficial owners

Business plan or company profile

Proof of business address

The Central Bank of Ireland regulates all banks operating in Ireland, ensuring they adhere to strict standards of customer protection and anti-money laundering procedures. As per the Payment Services Directive 2 (PSD2), implemented in Ireland through the European Union (Payment Services) Regulations 2018, banks must also provide secure online banking services and allow for third-party access to account information with the account holder’s consent.

It’s worth noting that the process can take several weeks, especially for non-resident directors or complex company structures. Banks are required to carry out thorough due diligence checks as part of anti-money laundering regulations, as stipulated in the Criminal Justice (Money Laundering and Terrorist Financing) Act 2010 and its subsequent amendments.

Set Up a Business Bank Account

When setting up your business bank account, consider the following factors to ensure compliance with Irish banking regulations and to choose the best option for your company’s needs:

Compare different banks and their offerings, considering both traditional banks and newer, digital-only banks. Each will have different fee structures, minimum balance requirements, and services.

Consider fees carefully. These may include monthly account fees, transaction fees, cash deposit fees, and international transfer fees. Some banks offer fee-free periods for new businesses, which can be beneficial in the early stages.

Ensure the bank can accommodate your international banking needs if applicable. This is particularly important if you’ll be dealing with multiple currencies or making frequent international transactions. The European Union (Payment Services) Regulations 2018 ensure that cross-border payments within the EU are treated the same as domestic payments in terms of fees.

Look at the online and mobile banking capabilities. Under the PSD2 regulations, banks must provide secure online access to account information and allow for third-party providers to access account information with the account holder’s consent.

Consider the availability of additional services such as merchant services, business loans, or financial advice. These services are regulated by various Irish and EU laws, including the Consumer Protection Code 2012 for financial advice and the European Union (Consumer Mortgage Credit Agreements) Regulations 2016 for business loans.

Prepare all necessary documentation beforehand to streamline the process. This typically includes:

Proof of identity and address for all directors and significant shareholders (as required by the Criminal Justice (Money Laundering and Terrorist Financing) Act 2010)

Certificate of incorporation (for limited companies)

Company’s constitution

Business plan or company profile

Proof of business address

Be prepared to provide detailed information about your business, including its nature, expected turnover, and source of funds. Banks are required to conduct thorough due diligence as part of anti-money laundering regulations.

Consider setting up multiple accounts if needed, such as a separate account for tax payments or for holding client funds if your business requires this. The Solicitors Accounts Regulations, for example, require solicitors to maintain separate client accounts.

Remember, while it’s possible to change banks later, it can be a time-consuming process, so it’s worth putting in the effort to choose the right bank from the start. Don’t hesitate to ask questions about the services offered and any aspects of the account you’re unsure about. A good banking relationship can be a valuable asset for your business as it grows and develops.

Streamlining Your Company’s Management in Ireland

Implement Robust Accounting and Financial Systems Use cloud-based accounting software integrated with Irish tax systems to automate financial processes and comply with the Companies Act 2014. This ensures proper record-keeping and adherence to accounting requirements.

Utilize Cloud-Based Collaboration Tools Cloud services are essential for remote teams, but ensure they comply with GDPR and the Data Protection Act 2018 to protect sensitive business data and maintain privacy standards.

Stay Compliant with Irish Laws and Regulations Use compliance tools like a calendar to track deadlines for filing returns with the Companies Registration Office (CRO) under the Companies Act 2014. This helps ensure timely submission of annual returns and other mandatory filings.

Outsource Non-Core Functions Consider outsourcing payroll, bookkeeping, and other non-core functions to save costs and focus on your core business. Ensure service providers comply with Irish laws like the Taxes Consolidation Act 1997 and the Data Protection Act 2018.

Implement Effective HR Practices Follow Irish employment laws such as the Employment Equality Acts 1998-2015 and the Safety, Health and Welfare at Work Act 2005. This ensures compliance and promotes good HR practices for recruitment, employee retention, and welfare.

Optimize Business Processes and Stay Informed Regularly review and improve business processes using quality management systems like ISO 9001. Stay updated on changes in Irish business regulations through resources like the Companies Registration Office (CRO) and Revenue websites.

How Easy Is It To Hire Personnel in Ireland?

Hiring personnel in Ireland is generally straightforward, with a well-educated workforce and flexible labor laws. However, there are several factors to consider to ensure compliance with Irish employment legislation:

Compliance with employment equality legislation is crucial. The Employment Equality Acts 1998-2015 prohibit discrimination in employment on nine grounds: gender, civil status, family status, sexual orientation, religion, age, disability, race, and membership of the Traveller community.

Understand the national minimum wage and working time regulations. As of 2023, the national minimum wage is €11.30 per hour for an experienced adult worker, as set out in the National Minimum Wage Act 2000 and subsequent orders. The Organisation of Working Time Act 1997 regulates working hours, rest periods, and annual leave.

You must register as an employer with Revenue before you can hire employees. This involves setting up a proper payroll system to manage PAYE (Pay As You Earn) and PRSI (Pay Related Social Insurance) deductions, as required by the Taxes Consolidation Act 1997.

Employment contracts are a legal requirement in Ireland. Under the Terms of Employment (Information) Acts 1994-2014, you must provide employees with a written statement of terms and conditions of employment within five days of starting work.

Be aware of employees’ statutory rights, including annual leave, public holiday entitlements, and parental leave. These are governed by various pieces of legislation, including the Organisation of Working Time Act 1997 and the Parental Leave Acts 1998-2019.

Ireland has a skilled workforce, particularly in sectors like technology, pharmaceuticals, and financial services. However, competition for top talent can be high, especially in Dublin.

Overall, while hiring in Ireland involves compliance with various regulations, the process is generally business-friendly. The availability of a skilled, English-speaking workforce makes Ireland an attractive location for many international companies.

Permits and Licenses

Depending on your business activities, you may need specific permits or licenses to operate legally in Ireland. Here are some common examples:

Food business licenses: If you’re operating any kind of food business, you’ll need to register with the Health Service Executive (HSE) under the European Union (Food Safety and Hygiene) Regulations 2020. Depending on the nature of your food business, you may also need additional licenses from your local authority.

Alcohol licenses: Businesses selling alcohol need a license from the Revenue Commissioners and approval from the District Court, as required by the Intoxicating Liquor Acts 1927-2018.

Environmental permits: Certain activities that may impact the environment require permits from the Environmental Protection Agency (EPA) under the Environmental Protection Agency Act 1992 and subsequent regulations.

Professional services licenses: Many professional services, such as legal, medical, or financial services, require specific licenses or registrations. For example, financial services providers must be authorized by the Central Bank of Ireland under the Central Bank Act 1942 and subsequent legislation.

Building and planning permits: If you’re constructing or significantly altering business premises, you’ll need planning permission from your local authority under the Planning and Development Act 2000 and subsequent amendments.

Music and copyright licenses: If you play music in your business premises, you may need licenses from the Irish Music Rights Organisation (IMRO) and Phonographic Performance Ireland (PPI) to comply with copyright laws.

Waste management licenses: Businesses that collect, transport, or treat waste may need a waste license from the EPA under the Waste Management Act 1996 and subsequent regulations.

Data protection registration: While not strictly a license, certain types of businesses that process personal data may need to register with the Data Protection Commission under the Data Protection Act 2018.

Obtain Relevant Licenses or Permits

To obtain relevant licenses or permits:

Identify the licenses required for your specific business activities. This may involve consulting with a legal advisor or industry association.

Contact the appropriate licensing authority. This could be a local authority, a government department, or a regulatory body depending on the license type.

Submit the required application forms and supporting documents. These can often be found on the relevant authority’s website.

Pay any associated fees. Fee structures vary widely depending on the license type and issuing authority.

Comply with any inspections or assessments. For example, food businesses may need to undergo hygiene inspections.

Await approval and issuance of the license or permit.

Ensure compliance with any ongoing requirements to maintain the license, such as regular inspections or renewals.

Identify the licenses required for your specific business activities. This may involve consulting with a legal advisor or industry association.

Contact the appropriate licensing authority. This could be a local authority, a government department, or a regulatory body depending on the license type.

Submit the required application forms and supporting documents. These can often be found on the relevant authority’s website.

Pay any associated fees. Fee structures vary widely depending on the license type and issuing authority.

Comply with any inspections or assessments. For example, food businesses may need to undergo hygiene inspections.

Await approval and issuance of the license or permit.

Ensure compliance with any ongoing requirements to maintain the license, such as regular inspections or renewals.

Register with the Data Protection Commission if necessary, as required by the Data Protection Act 2018.

Implement appropriate data protection policies and procedures in line with the General Data Protection Regulation (GDPR) and the Data Protection Act 2018.

Ensure compliance with the GDPR’s principles of data processing, including lawfulness, fairness and transparency, purpose limitation, data minimisation, accuracy, storage limitation, integrity and confidentiality, and accountability.

Appoint a Data Protection Officer if required under Article 37 of the GDPR.

Regularly review and update your data protection practices to ensure ongoing compliance.

Implement appropriate technical and organizational measures to ensure the security of personal data, as required by Article 32 of the GDPR.

Ensure you have a process in place for handling data subject access requests and other data subject rights under the GDPR.

Depending on your business activities, you may need to comply with additional legal requirements such as:

Consumer protection laws: The Consumer Protection Act 2007 and the European Union (Consumer Information, Cancellation and Other Rights) Regulations 2013 set out key consumer rights. These laws cover areas such as unfair commercial practices, misleading advertising, and consumer contracts.

Intellectual property rights: The Patents Act 1992, the Copyright and Related Rights Act 2000, and the Trade Marks Act 1996 govern intellectual property protection in Ireland. If your business involves creating or using intellectual property, it’s crucial to understand and comply with these laws.

Health and safety regulations: The Safety, Health and Welfare at Work Act 2005 sets out the main provisions for ensuring the safety and health of workers. Employers have a duty to ensure, so far as is reasonably practicable, the safety, health, and welfare of their employees.

Environmental regulations: The Environmental Protection Agency Act 1992 and various waste management regulations may apply to your business, particularly if you’re in manufacturing or deal with potentially hazardous materials.

Sector-specific regulations: Certain industries have additional regulatory requirements. For example, financial services are regulated by the Central Bank of Ireland, while food businesses must comply with food safety regulations enforced by the Food Safety Authority of Ireland.

It’s advisable to consult with legal professionals to ensure full compliance with all relevant laws and regulations specific to your business activities.

Final Thoughts

Establishing a business in Ireland offers numerous advantages, including a favorable tax regime, access to the EU market, and a skilled workforce. However, navigating the legal and regulatory landscape requires careful planning and attention to detail.

Key points to remember:

Choose your business structure carefully, considering factors like liability protection and tax implications.

Ensure compliance with all registration and licensing requirements.

Stay up-to-date with tax obligations and filing deadlines.

Familiarize yourself with Irish employment law if you plan to hire staff.

Consider seeking professional advice for complex legal or financial matters.

While the process may seem daunting, Ireland’s business-friendly environment and supportive ecosystem for startups make it an attractive location for entrepreneurs. By following this guide and seeking professional advice when needed, you can set up your business efficiently and compliantly in Ireland.

Frequently Asked Questions on Starting a Business in Ireland

Q: How long does it typically take to register a company in Ireland? A: Standard registration usually takes 5-10 working days, while fast-track registration can be completed in 5 working days for an additional fee.

Q: Do I need to be an Irish resident to start a business in Ireland? A: No, but you need at least one EEA-resident director or a non-EEA resident director bond.

Q: What is the minimum share capital required to set up a company in Ireland? A: There is no minimum share capital requirement for private limited companies in Ireland.

Q: Can I open a business bank account remotely? A: While some banks offer online applications, most require at least one in-person meeting to verify documents and signatures due to anti-money laundering regulations.

Q: What are the main tax rates for businesses in Ireland? A: The standard corporate tax rate is 12.5% on trading income and 25% on non-trading income.

Q: Do I need to register for VAT immediately? A: You need to register for VAT if your turnover exceeds or is likely to exceed €75,000 for goods or €37,500 for services in any 12-month period.

Q: What are the main types of business structures in Ireland? A: The main types are Sole Trader, Partnership, and Limited Company (including Private Limited Company and Designated Activity Company).

Q: Are there any grants or financial supports available for new businesses in Ireland? A: Yes, various grants and supports are available through agencies like Enterprise Ireland and Local Enterprise Offices.

Q: How often do I need to file tax returns in Ireland? A: Companies must file Corporation Tax returns annually, while VAT returns are typically filed bi-monthly or quarterly.

Q: What are the main employment laws I need to be aware of when hiring in Ireland? A: Key areas include employment contracts, working time regulations, minimum wage requirements, and equality legislation as outlined in the Employment Equality Acts 1998-2015 and the Organisation of Working Time Act 1997.